Heston library added to Quantlab

The Heston model has been around for a good 25+ years. Why would we add a this model to our library now?

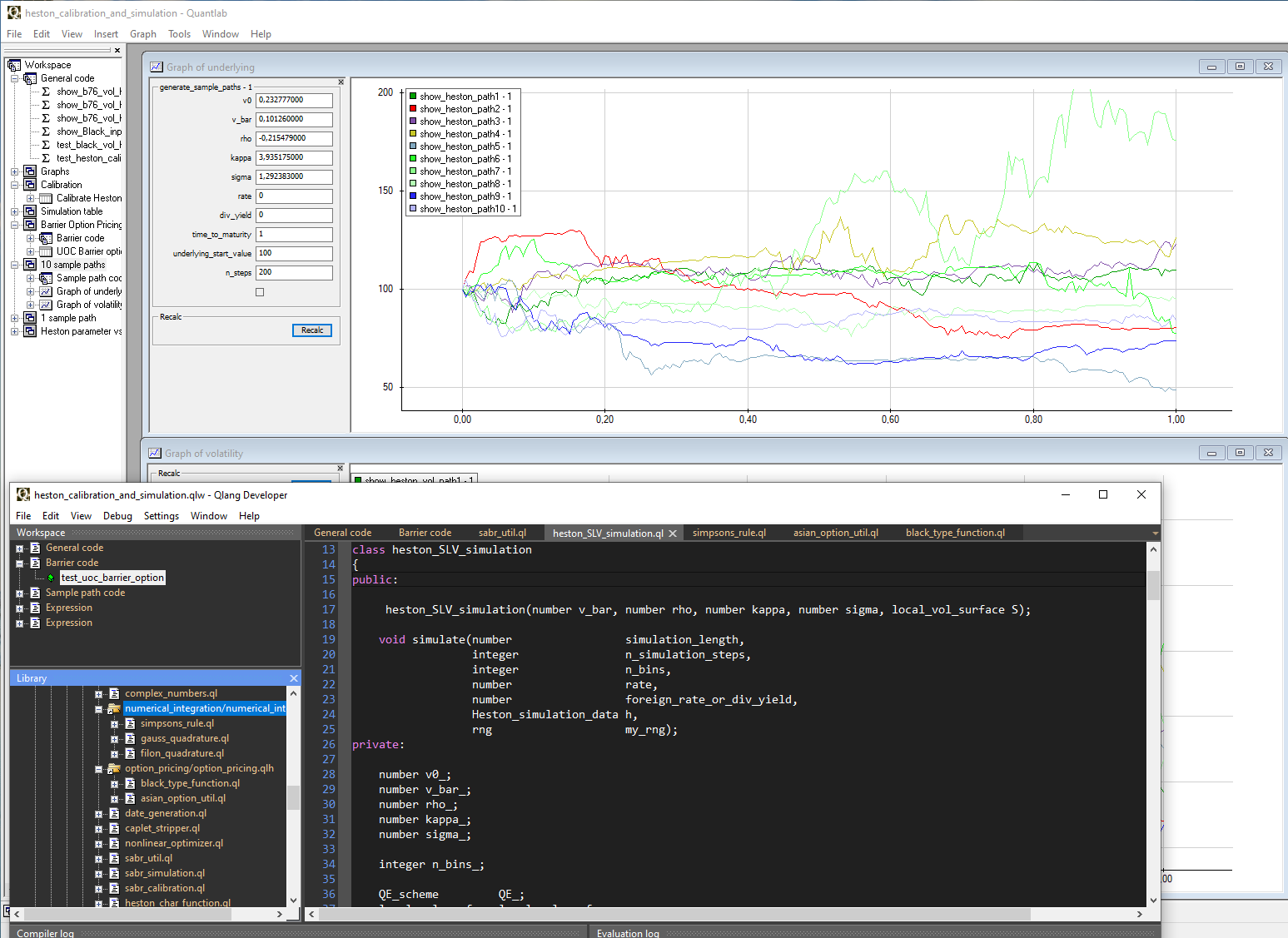

In recent time there has been some ground breaking research into numerical stability when calibrating models such as the Heston. We have chosen to implement a number of those recent advances and are very pleased with the results.

Note that you may run all Qlang libraries as well as your own from other environments directly, such as Python, Excel, C# and using RestAPIs.

By means of pricing by Fourier Transforms, Contour Deformations, and various methods of exponential Quadrature, we have created a fast, robust and highly accurate calibration library.

We have also made extensive use of more exact methods of pricing Black prices and Black implied volatilities which are a necessity for fast and reliable convergence of the optimizers.

For more information about Heston pricing in Qlang/Quantlab. Please call an Algorithmica sales rep.